Australia’s 20-year-long economic party, funded by China, may be drawing to a close, with consequences for federal and state budgets, superannuation returns and living standards generally.

The iron ore price is the most obvious pointer to China’s declining demand for Australia’s raw materials: it has come down from an extraordinary peak of US$144 a tonne at the beginning of January to a spot price of US$92 this month, and the fall is expected to continue.

It is amazing that it has remained high for as long as it has, given that the construction of housing in China—traditionally accounting for 30 percent of its domestic steel use—has turned down since the biggest builder, Evergrande, struck financial trouble in 2021.

The subsequent collapse of Evergrande and other major builders has sapped Chinese consumer confidence, since housing is by far the biggest destination for household savings. Authorities sought to offset the housing decline by advancing further support to manufacturing and seeking growth in export markets.

China’s exports rose from an annual average of US$2.5 trillion between 2018 and 2020, reaching US$3.4 trillion over the past three years. While this has brought protest and retaliatory tariffs in many advanced nations, Australia was able to piggy-back on China’s export boom.

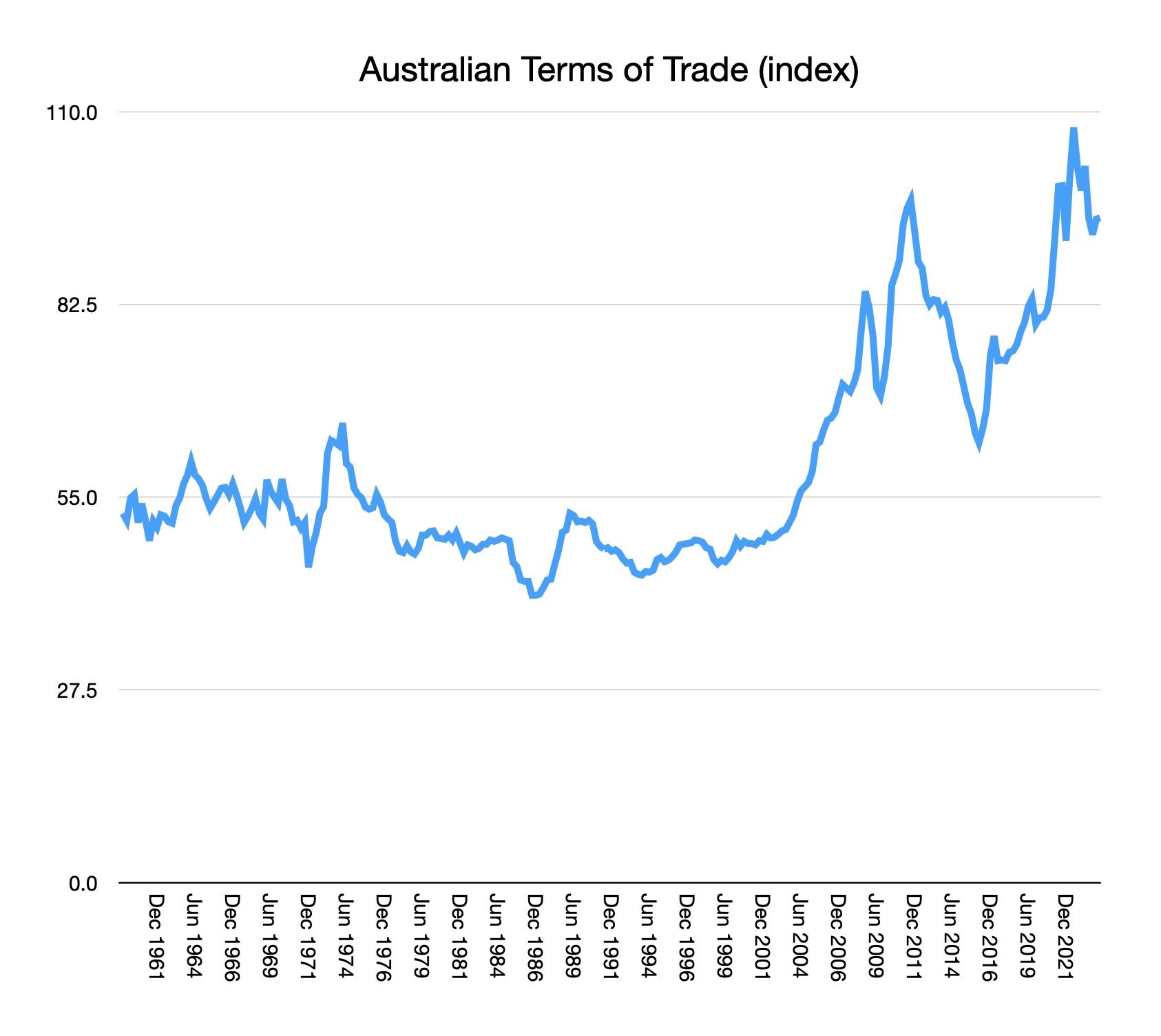

The prices Australia receives for its exports, relative to what we pay for our imports, have never been better than over the last two years. Our returns from trade have been even greater than during the peak of the resources boom in the early 2010s. The only other episode in Australia’s history that comes close was the wool boom during the Korean War in 1951, but that lasted barely a year.

The benefits of the bonanza have been widely spread. The resource companies and their shareholders, including most Australian superannuation funds, have achieved extraordinary returns. Resource company tax payments have delivered healthy budget surpluses to the federal government, despite its spending rising to the highest level in almost 40 years. Royalties have boosted the finances of the West Australian and Queensland governments.

The public at large gains not only from the spending on government services but also from cheaper imported goods with the strength of export prices boosting the value of the Australian dollar.

These extraordinary returns to Australia from trade have occurred while global trade has been flat. There has been no growth in world trade volumes since the beginning of 2022, and average trade prices are lower. The International Monetary Fund attributes the weak global trade performance to the rise of protectionism and fragmentation, as trade within geopolitical blocs rises while trade between them falls.

The strength of Australia’s returns from trade over the past two years was not expected. Treasury has repeatedly predicted an imminent slump in iron ore prices to US$55 to US$60 a tonne (with similar falls in coal prices) in every budget since at least 2017.

But the Chinese authorities’ preference for stimulating their economy through subsidies to manufacturers, rather than through tax cuts or payments to consumers, has kept the rivers of cash flowing to Australia’s miners.

Although the past few years have been exceptional, Australia’s Chinese bonanza is now into its 20th year. Until the early 2000s, China’s economic growth was driven by light industry, but huge investments in infrastructure and heavy industry brought explosive growth in demand for Australian resources from 2004 onwards.

Until then, it was thought that Australia’s dependence on resource exports would bring ever-weaker returns from trade: from the mid-1970s until the early-2000s, the average returns from exports were gradually falling while the average cost of manufactured imports was rising. This was the outlook facing the Howard government for much of its term.

Instead, there has been a remarkable rise in Australian living standards. In 2004, Australia’s income per person ranked 23rd, behind the United States, all the major countries of Europe, Britain and Japan. It now ranks ninth and has overtaken every larger country except the US (excluding tax havens), according to World Bank data.

But China is now bumping up against the limits of its export-driven economic model. Export growth is slowing and steel production is falling. Steel output in July was down 9 percent from the previous month leading the chair of China’s biggest steelmaker, Baowu Steel Group, Hu Wangming, to warn staff at the company’s half-year meeting that conditions were like a ‘harsh winter’ that will be ‘longer, colder and more difficult to endure than we expected’.

It is a chill that will likely be felt in Australia. Already, Treasurer Jim Chalmers is warning that the federal budget balance will deteriorate, while the impact of weaker exports will flow through to superannuation returns, the value of the Australian dollar and the cost of imported goods. Living standards will suffer.

For the most of the past 20 years, it has been a seller’s market for Australia’s resources. The many efforts of China’s authorities to weaken the markets for major commodities have failed. How China will exploit its market power once it becomes a buyer’s market is an open question.